Understanding The Purpose Of Life Insurance In Retirement

How Retirement Reshapes The Role Of Life Insurance

For many families, the purpose of life insurance is straightforward in the early years: protect a paycheck, keep the household running, and make sure dependents can stay on track if something happens. Near retirement, the math changes. Income may be less dependent on wages, but new needs can appear that still call for dependable liquidity.

As mortgages shrink and children become financially independent, the “income replacement” reason for coverage often fades. In its place, retirees may use life insurance to create cash on demand at death, support a surviving spouse’s financial stability, equalize an estate among heirs, or make a meaningful charitable gift. The shift is subtle but important, because it moves the conversation from “How much coverage is enough?” to “What role do we need this policy to play now?”

Matching Policy Structure to Your Planning Priorities

Different policies support different parts of the purpose of life insurance. The right choice depends on whether you need coverage for a defined period, for a lifetime, or for a specific planning objective like estate liquidity.

Before comparing options, it helps to be clear on the “job” you are hiring the policy to do. Once that is defined, the differences between term and permanent coverage become much easier to evaluate.

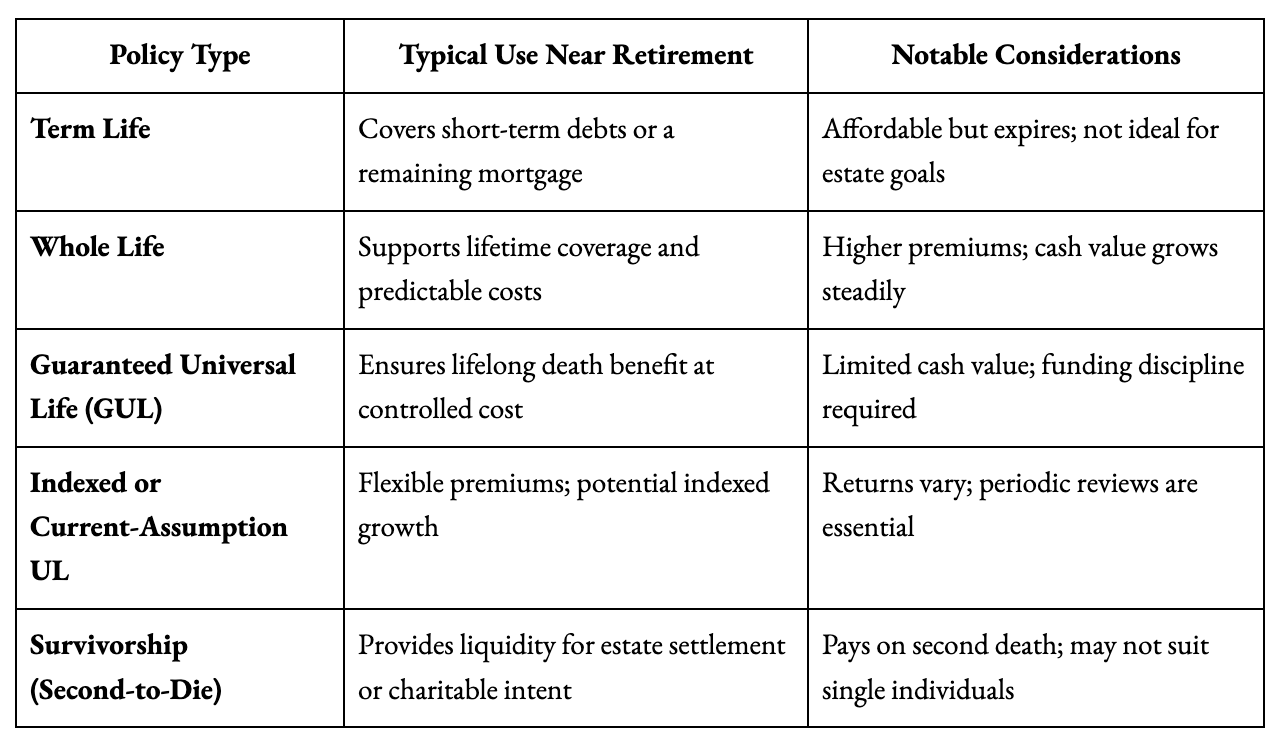

How Common Policies Stack Up For Retirement Goals

The table below outlines how common policy types are typically used near retirement, along with practical considerations that often matter in real-world planning.

A common planning preference near retirement is to focus on policies that deliver a reliable death benefit without requiring unnecessary complexity. In many cases, GUL or carefully funded universal life can be positioned for lifetime protection when the primary goal is liquidity at death, rather than building significant cash value.