Episode 19: 5 Retirement Planning Mistakes & How To Avoid Them

In this episode, we're going to talk about five common retirement planning mistakes. Roger and Jake spend a lot of time preparing people for retirement and have seen a lot of mistakes that pre-retirees, and even retired clients, struggle to overcome. Let's find out more about these mistakes and most importantly how to avoid them.

First on our list is sequence of returns. We look at what returns are coming in and when they happen during your retirement years. Then we’re going to talk about coordinating those returns how to manage your cash. How much do you need in the next one, two, or maybe even three years? Next, we're going to get into some of the mistakes that relate directly to investor behavior. Missing those best 40 or 10 market days, out of a 20-year period.

Next, a lot of bad decisions relate to trying to time the market. Maybe you get a little bit nervous and don’t feel as prepared as you should. And lastly, we’re going to look at unrealistic expectations; what should we be earning at a certain level of risk? Those are the things that you need to be thinking about.

And most people say, “well, Roger, I'm only thinking about how much I'm going to spend on vacation this year.” That's okay. We want you to do that, but you're going to have to look at some of these other things.

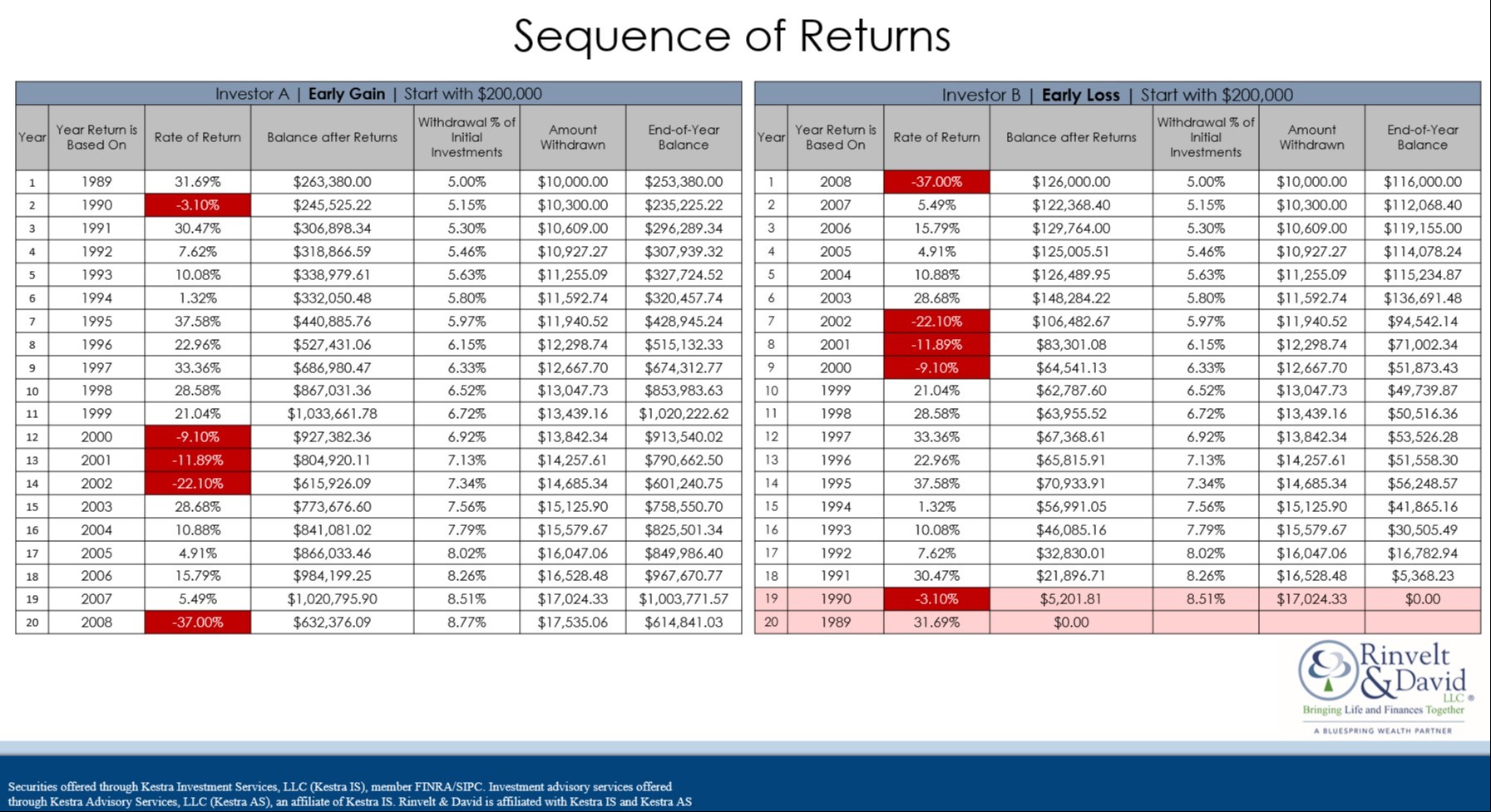

So, let’s get into sequence of returns. What does that actually mean? It’s when you experience losses from market fluctuation. And when we look at this, the key thing is you don't want to take big hits, big drawdowns in your portfolio early on in retirement. And when you look at the chart that we've got here, we've got a comparison.

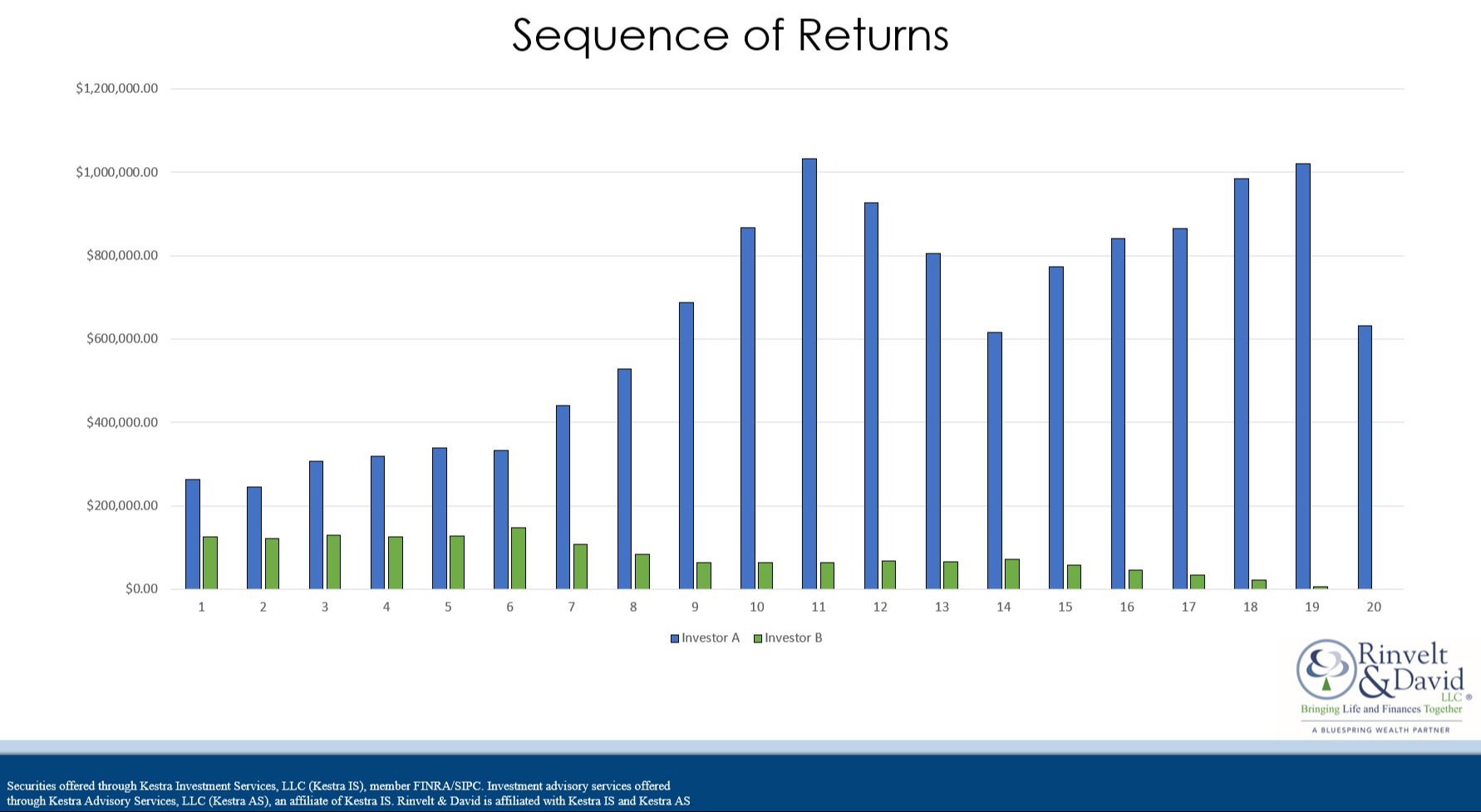

The left shows what happens when we don’t take big hits at the front end of retirement. And if you look at this chart all the way through this 20-year period, you'll see that not taking big hits at the front end and still taking your withdrawals, our example client didn't run out of money. There's still some money left over at the end of this 20-year period.

Now, if look over to the right at the other chart, all we did here is we just flipped this 20-year period. We put the losses at the front end. Everything else remains the same - the withdrawal rate, the average rate of return over time, it's just a matter of when those losses occurred. So, what happens when this client took losses early on in retirement? They outlived their money. So what do you do to try to avoid that? You've got to manage your cash, and manage it effectively.

We watch sequence of returns and cash management closely when somebody just begins their retirement because we understand the negative impact improper management can have over the long haul. But there's another component that goes along with some of these mistakes and it's very common.

Emotions. We can create your financial plan, put together the perfect portfolio allocation for you based on your risk tolerance, your time horizon, based on short, intermediate, long-term needs, put together the perfect portfolio for what we believe you need to be invested in longer term. And then emotion gets in the way; biases that you may have mentally that make you feel like if the market's performing poorly, you have to take some sort of action.

And oftentimes, that means people are going to start implementing a market timing approach to managing their money, which we don't like to do. We want to invest long term because you can see in the chart below what can happen if you try to time the market. When you're timing the market, you have to get lucky twice.

You have to hope that you move to cash when the markets at a high and then you move back into the market once it hits a low. All so you miss out on all of that decline in the portfolio.

What usually happens when timing the market, is people take a lot of the hit on the front end of a market downturn. People think, “oh my gosh, the market is falling. I'm going to move to cash.” They have now locked in that loss. And then they’re way too late getting back into the market because they want to see a sustained recovery after these hits. Because they’re nervous.

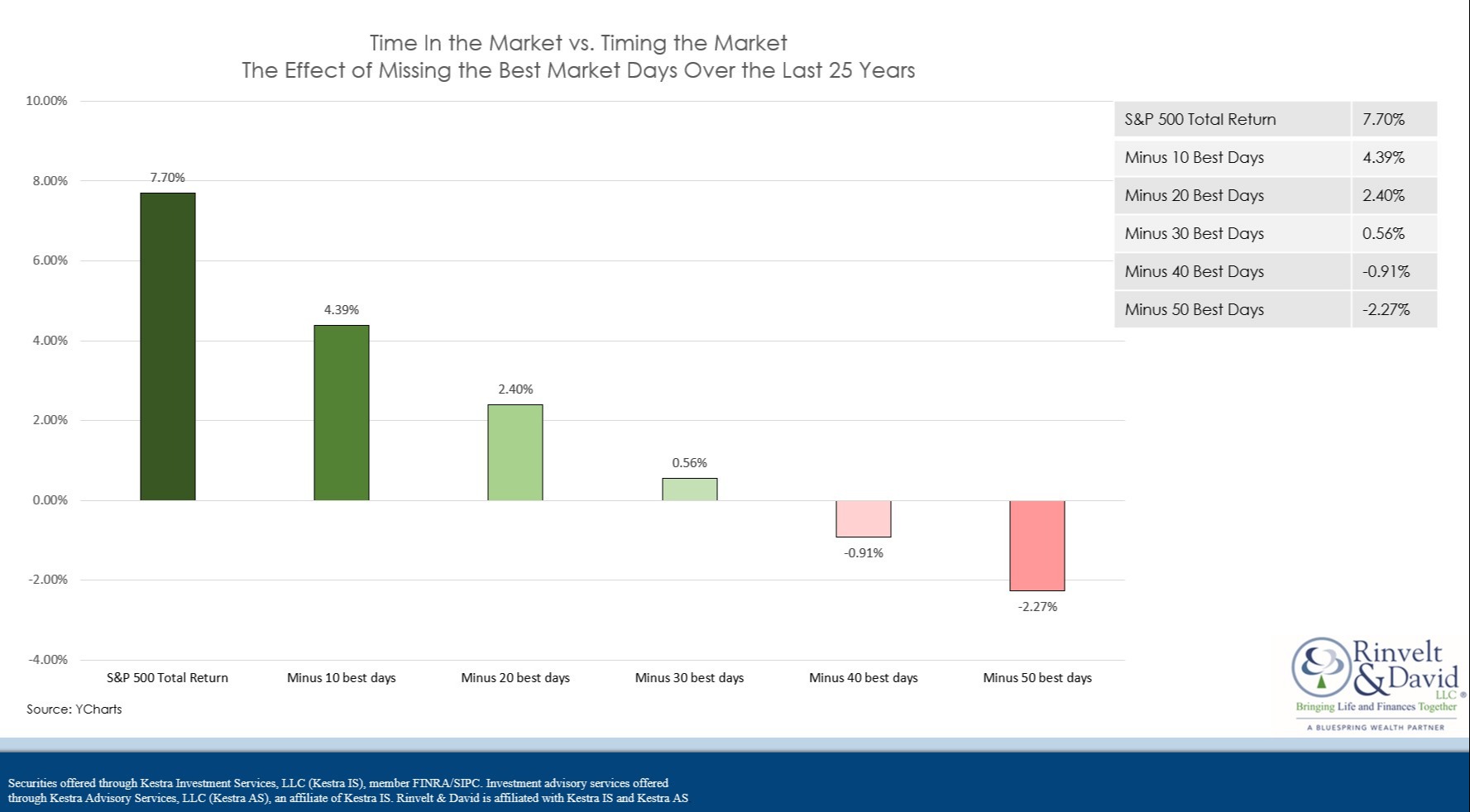

That emotional decision-making, over time impacts your return. We're looking at this chart at market returns over a 25-year period. Missing out on a few days’ worth of the best performance can impact your average annual return. If you miss the best 10 days, your return drops from 7.7 percent annualized to 4.39. Where if you miss the best 40 and 50 days over that 25-year period, you now have a negative annualized rate of return.

And when do those best days usually happen? In the initial portion of the recovery. It's usually the first 30 days after a big downturn. That's why our belief is that when you're investing, it's about time in the market, not timing the market.

And that's where we come into the mix. Where we're trying to help clients manage those emotions, manage those expectations, and create a portfolio that's allocated so that in an all-weather approach, there's going to be stuff that's not getting hit as hard when the markets are performing poorly.

We don't know when things are going to change. We don't know how extreme swings will be. But we do know that we're planning for those things. There should always be something in your portfolio to handle any type of weather.

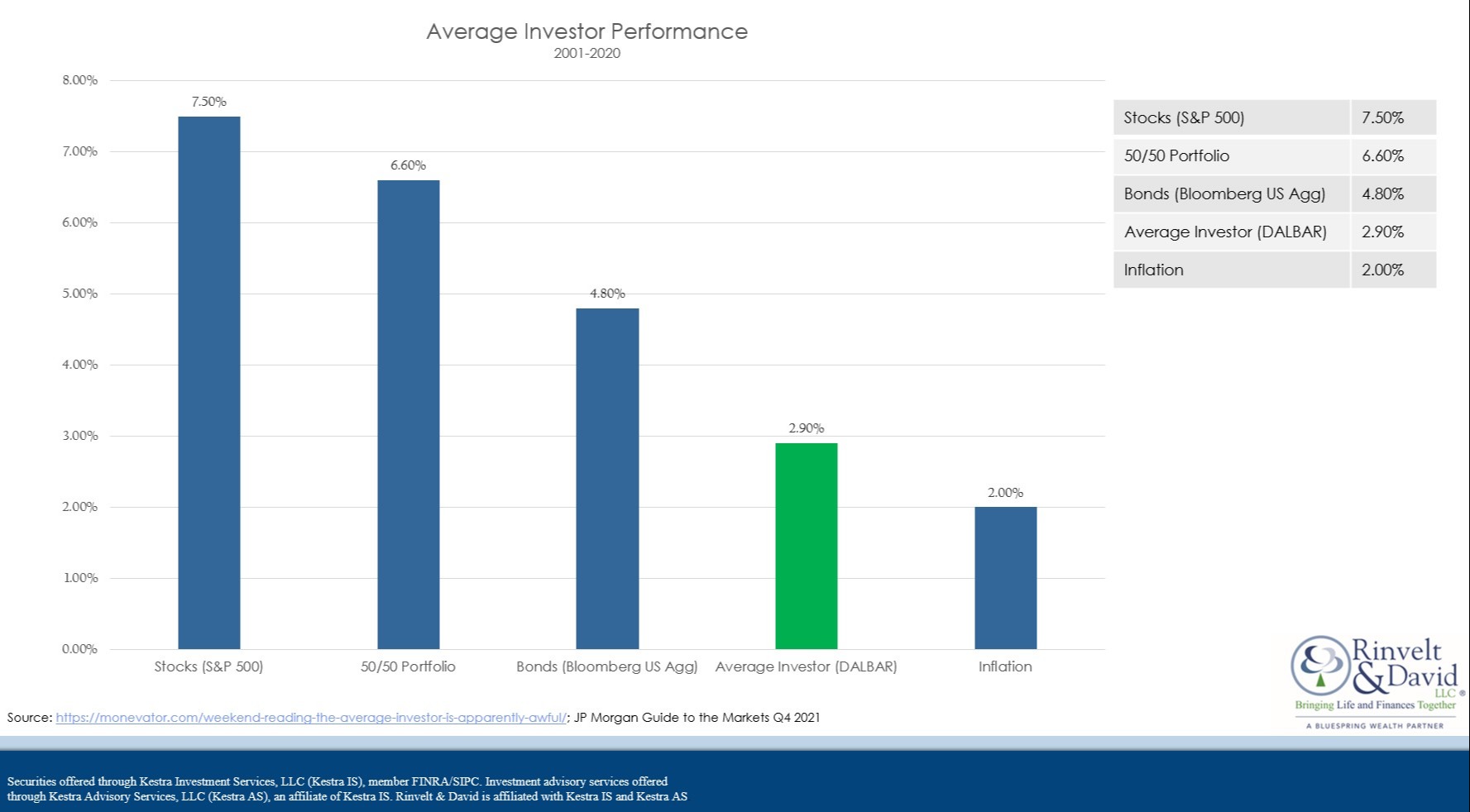

Let’s look at another chart that shows the impact timing the market out of a sense of fear or needing to exert control over your losses. Over a 20-year period, from 2001 to 2020, we look at some of the returns of the major asset classes compared to what's called the average investor. Every year, DALBAR runs a study where they calculate the returns of an average investor where those returns are negatively impacted by market timing and some poor decision-making when managing the portfolio.

As you can see over this 20-year period, the average annual performance of the S&P was seven and a half percent. Not ten percent. The aggregate bond market was up 4.8 percent and then you've got your lowly average investor earning 2.9 percent on average annually.

There's actual math and studies that shows making emotional decisions when it comes to managing a portfolio can compound and really impact your return. And you want to try to stick to your financial plan.

When you deviate from the financial plan, either with us or with another advisor, this is what happens. An average of 2.9 percent rate of return. And if we asked any of you, “hey, what's the key to investing?” We know you would know the answer. Buy low, sell high. Instead, people do the opposite. Sell low, buy high. Because of emotional decision making.

On of the other things that goes along with the most common mistakes is unrealistic expectations. Let’s say I've got a million dollars, and my expectation is to make 10% on that money - which we just saw on the chart isn’t realistic. But still, I think, “hey, I’ve got a million dollars and I’m going to make 10% on that money. That’s a hundred grand a year plus my Social Security. Man, I'm going to live the life that nobody lives. It's going to be fantastic.”

But the key missing component, with attempting to achieve a 10% rate of return, is looking at an appropriate level of risk you should be taking with investments. You've got to watch what your risk factor is. You've got to manage your cash because your days of accumulation? They're done.

You really are going to have to look at what your expectations are and what do you have. And a lot of times those expectations, as far as they relate to the rate of return, are probably going to mislead you into thinking that you have enough saved. Look back at the last chart – the S&P earned seven and a half percent over a 20 year period.

Over the 25-year period, it was 7.7. If you think that you're going to earn 10%, you’ll have to invest in really risky stuff. We're talking about emerging markets, or small cap growth stocks. You’re adding a lot of risk to your portfolio.

It’s important to get your hands around and understand what sequence of returns means and what its impact could be. Take the emotion, as much as you can, out of what's going on in your decision-making and try to put together an all-weather approach. And make sure that your expectations are realistic. And the only way you're going to be able to do that is if you do proper planning.

Understand what the common retirement mistakes are, ask questions about them, and try to avoid them as much as possible. Once you start making that financial plan and you've kind of looked at all these things and what the impact could be, it's only then that you're really bringing life and finances together.

Thanks so much for reading along with us and learning about retirement planning mistakes and how to avoid them today. For questions about our financial services or finances in general, send us an email, give us a call, and of course, please like and subscribe to our podcast and stay tuned for our next episode.