Episode 17: Social Security Q&A - Take Early or Delay?

In this episode, Roger and Jake, will be discussing a topic that comes up in every financial planning meeting, Social Security, a benefits program that we've all paid into through our working years and that we are all duly owed and even expect as part of our retirement income. It's an important topic, and we’re excited to share this valuable information with you.

Well, we've paid into this system for a long period of time. It's one of the things that clients talk about so much. Is it going to be around? What am I going to get? What are the things I need to consider?

We’re going to talk about two of the key components that Social Security is based on and then we're going to talk about the two big questions - the first one is do I take it early? Does it make sense? The second is should I delay it?

To answer these questions, the two key components that everybody needs to understand are the FRA and the PIA.

The FRA is our Full Retirement Age. It used to be 65 for everybody, then they changed it, back in the early 80s, and now for Jake and I and folks in our age groups, we're at 67.

The PIA is the Primary Insurance Amount and that's the value of your benefit at your full retirement age (FRA). Those are the two things that everything in Social Security is calculated around.

Those are two key components that you need to be aware of as you begin to look at Social Security and start making some of these key decisions. So do we take it early?

When we advise clients, it really is plan specific as to when is the optimal time to take Social Security and we'll look at different options. But a lot of the reasons why people may start taking their Social Security early involve needing the income right away. When we look at their financial plan, if they're retiring early and they don't have any other income sources, they may need that income.

They may also decide, hey, I may not need the income right now, but it is owed to me, I may as well start taking the income now. I might want to invest it. Instead of just having it sit there and not earn any interest, let me start receiving this income and investing it in some sort of investment vehicle so it can earn a little bit more, right?

You may also want to start taking yours early if it behooves you to delay your spouse's benefit. Your spouse may have a larger benefit based on their working credits, the amount that they've paid into the system. It may be more beneficial to delay theirs so they get more of an increase in their pay, so you may want to take yours sooner.

And the biggest thing, and this is when it comes to sources of income in retirement, taking your Social Security alleviates the need to withdraw more from your retirement savings on the front end of retirement. So the ability to forego taking excess withdrawals out of your IRA or non-qualified investment account allows more money to stay in that account and compound and grow further into retirement. We always like to say your spouse or your heirs can inherit your investment accounts from you. They cannot inherit your Social Security from you. So it's something that allows you to keep money in your invested portfolio and keep it growing.

And Social Security doesn't do a good job of explaining all of this. If you go to a conference or a webinar or workshop with Social Security, they don't bring that into the mix. They're not talking about that at all. It's our job as the financial advisor to do that, right?

So as financial advisors, we do the calculation on the cash flow. We'll always do a breakeven and we've got an example for you just to see what an example of a breakeven might look like if you are deciding to take Social Security early.

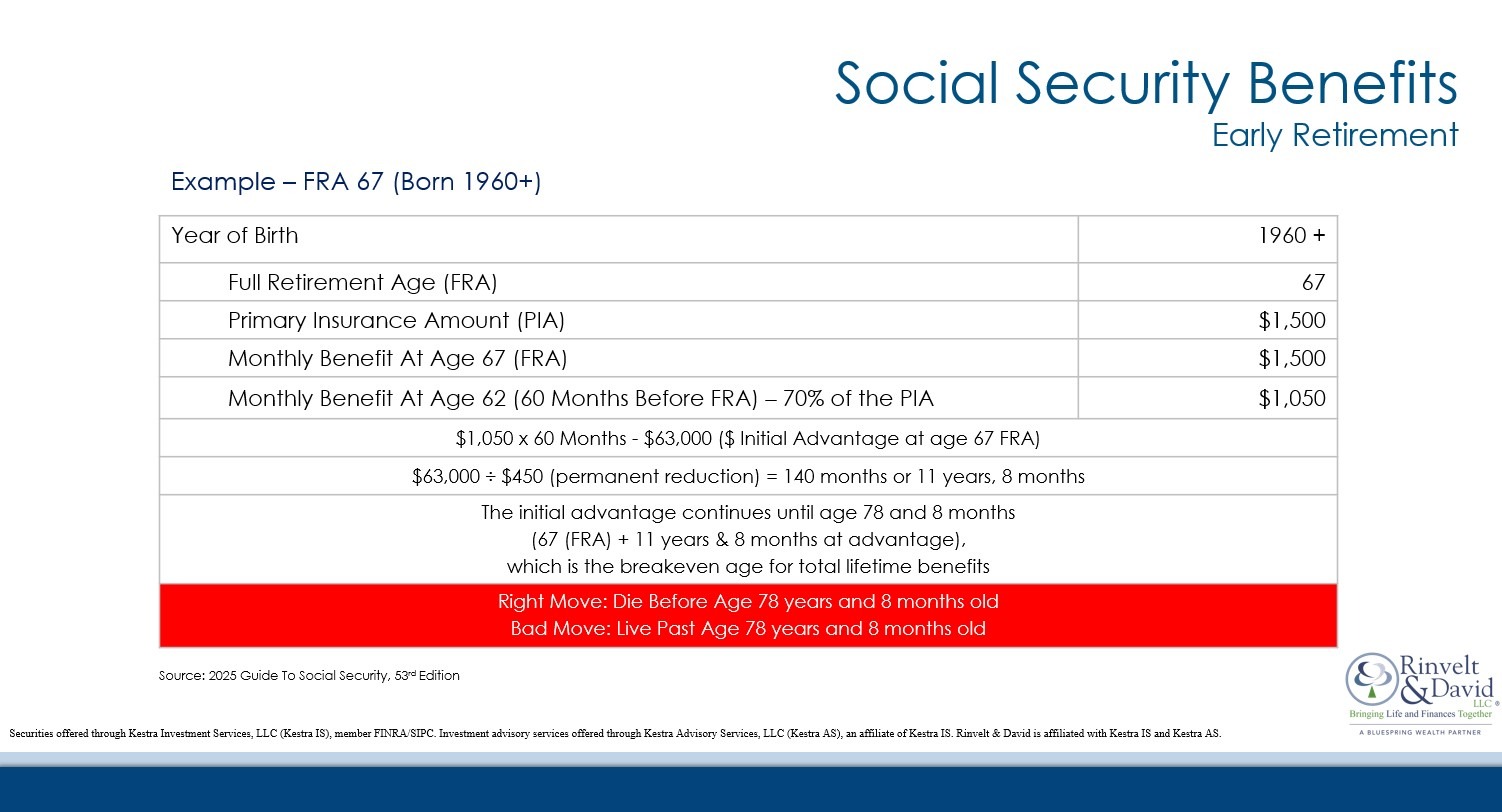

Now this is really everything in a vacuum here when we're looking at the numbers, but the example we have is an individual with a full retirement age of 67, which really is anyone from Roger's age to even my age. We're all kind of stuck in this age of 67. We’ve got an individual whose PIA, the primary insurance amount, at FRA, full retirement age, is $1,500, but you can see that if they decided to take their Social Security benefit early, they're going to receive $1,050 a month, right? When you look at the math, if you decide to take it early, you need to essentially, and we always joke, you need to know when you're going to die, wink, wink, to know if you're making the right decision or not. This was the right move if you passed before 78 and 8 months. If you lived beyond that point, then it was not a good move. So you need to have the foresight, we joke, but that's really what it comes down to. If you're going to take it early, in a vacuum, this is the analysis behind the breakeven.

Now on top of that, you need to factor in on taking early if you're going to keep working. If you're going to retire from your main job but do some part-time work, if you're going to go be a starter at a golf course, whatever it may be, if you're underneath that full retirement age, you have to make sure you know how much you're going to earn. In 2025, the earnings limit is $23,400. So if you know that you're going to earn close to or more than that, it may actually behoove you to delay and not take Social Security early because you don't want your benefits to be reduced.

So there's a lot of different factors that go into this.

And if you run into a situation where, oops, I didn't think I was going to have any earned income and now I do, and maybe you're over that threshold that Jake was talking about, you're going to definitely want to get a hold of Social Security and let them know in advance, right? Because they're going to start reducing your benefit.

What do they reduce that by? It's like $1 for every... $2 earned, every $3 earned. Over the threshold. Over the different thresholds.

Remember, your benefit is taxable - either 50 or 85% of it will be taxable, but then there can be reduction on top of that if you earn too much income. So we want to try to coordinate it as best as we can.

A common misconception regarding taking your benefit early is that people think in this example, from age 62 until age 67, I'm going to receive $1,050 a month. But once I reach that full retirement age, 67, now I'm going to get that increase to $1,500. Well, that's not the case. You are locking in that lower payment for the rest of your life. It's a permanent reduction. So you’ve got to make sure if you're going to take it early that it is the correct decision. And the only way you know that is through planning.

So just be careful when it comes to saying, I want to take it early. We’ve had a lot of clients that will say, I'm taking it early. I paid into this thing and I want my money, right? Well, you've got to do a little bit more planning and coordinating. And I'm with you. I'm with you. We want to receive the benefit of all the years of paying those taxes, but you’ve got to be careful because it may not make sense to do it.

Then we get to the opposite big question, do I delay?

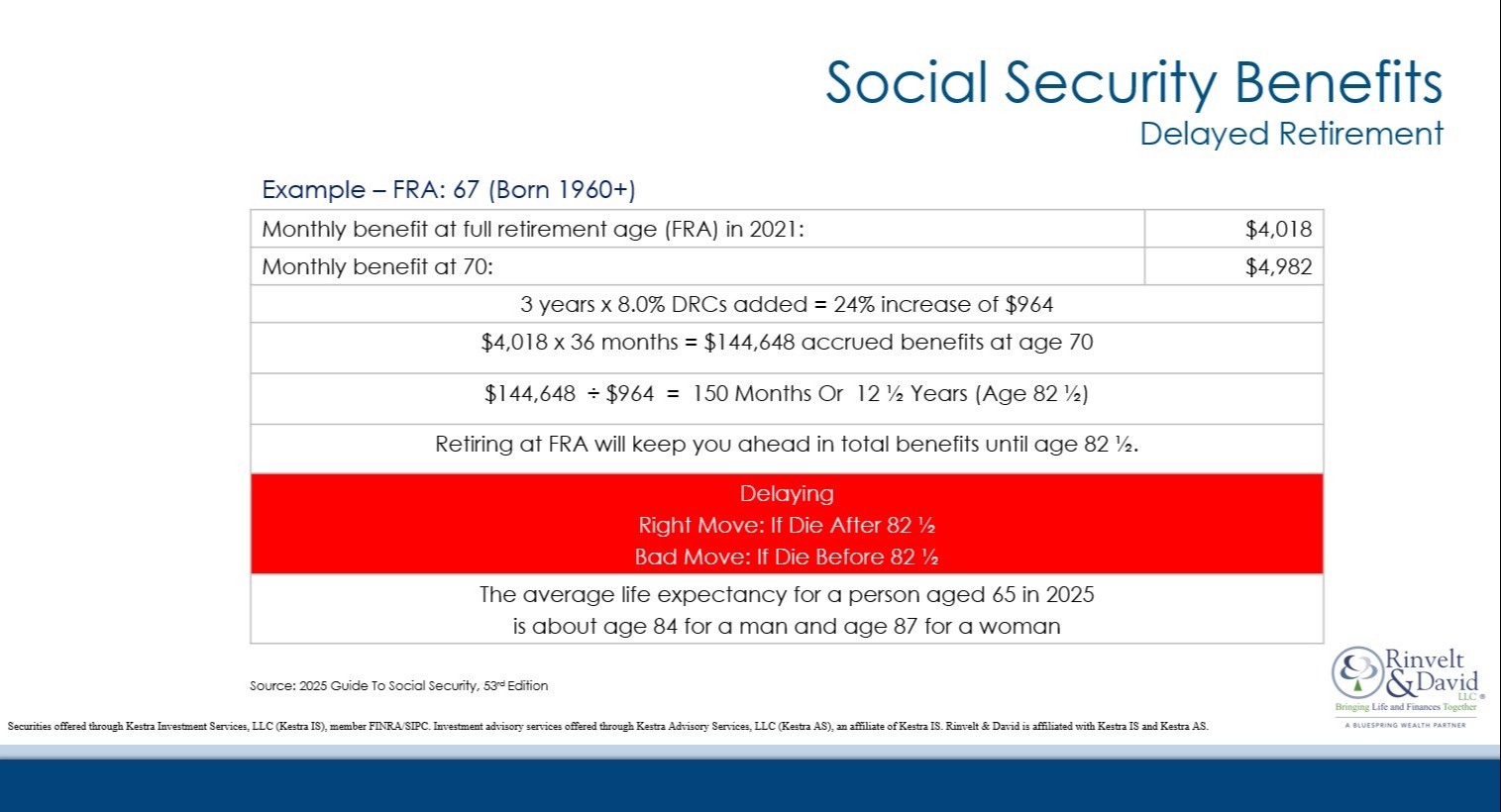

There's this attractive little thing called DRCs, Delayed Retirement Credits. And they represent an 8% non-compounded bump every year that you delay past your full retirement age. So if I delay the 3 years past my FRA of 67, I could have an increase that's roughly around 24%. Pretty awesome, right? But there's a lot of other factors to consider other than just these Delayed Retirement Credits.

Maybe you’re still working. When you get to full retirement age, you can make as much money as you want and not have to worry about your benefits on Social Security being reduced. Now in the year that you turn full retirement age, there's a little bit of a calculation, there's an income threshold in that year, you have to be concerned about, but we're not going to get into that here. When you're looking at beyond your full retirement age, make as much money as you want and you can take your Social Security benefits with no reduction. So that's one thing to consider. But if you're earning income and you don't need it, why take it? Get the delayed retirement credits.

Maybe you want to leave a larger benefit to your spouse. So if you have a large benefit and your spouse maybe has a small benefit, when you pass away your spouse is going to maybe receive the larger of the two benefits. So perhaps you want to enhance that benefit. That's another thing.

Maybe you're going to try to coordinate your spouse taking their benefits and you delaying while you're alive.

For what reason? To have increased income while both of you are retired. So the other thing too is maybe you just don't want to take the benefits and have it subject to higher income taxes. Because you're still earning income.

So those are things to consider. It's not just this real easy decision because your neighbor over the fence told you, oh, I did it, so you really need to do it. You've got to do the math.

When we look at this chart, we're looking at someone who has a full retirement age of 67 and they're receiving at their full retirement age, their PIA is $4,018. Now, they delay until they're 70 and then start taking their benefits. That benefit goes north of $4,900. So again, when we're looking at this in a vacuum, there's a calculation that we provided and you can very easily plug in those numbers. When did it make sense in this scenario to delay? Well, it was the right move if you live past 82 and a half years old.

So again, it comes back to this magical number of I know when I'm going to die and I'm going to make the right move. We say that kind of jokingly, but consider, do I have longevity? My grandparents, my parents, right? Do they live well into their 90s? This could be a determining factor in whether you decide whether you want to delay or not. But there's a lot to think about and discuss with your financial team.

You have to do the math. You have to look at the breakeven, not only like in the chart that we provided, but also in your financial plan, looking at the impact of your investment savings. That's one of the key things to look at.

And if that breakeven is way out there, maybe in your late 80s or even 90s, well then you've got something to consider. You need to look at your options before you make the decision based upon rule of thumb. When you're coordinating your benefits and looking at all these different factors as it relates to Social Security and incorporating them into your plan, that's when you know that you've truly done the work to bring life and finances together.

Thanks so much for reading and for learning about Social Security with us today. For questions about our financial services or finances in general, send us an email, give us a call, and of course, please like and subscribe to our podcast and stay tuned for our next episode.