There are plenty of ways to talk about money and how we use it. Cash flow. Nest egg. Slush fund. Finances. But “budget” is the word that tends to make people tense up.

That reaction is understandable. Looking closely at where money goes can feel uncomfortable, especially when prices keep changing and every month seems to bring a new expense. But a budget does not have to be a scary or complicated exercise. At its simplest, a budget is an estimate of income and expenses over a period of time. More importantly, it is one of the most useful ways to see whether your money is supporting the life you want now and the goals you are building toward later.

Key Takeaways

Budgeting is not only for people who are in debt or trying to cut back. It is a cash-flow tool that can help you spot habits, prepare for surprises, and make larger financial decisions with clearer numbers in front of you.

A budget can show where small spending patterns are affecting larger goals.

Cash-flow planning helps connect today’s choices with future needs.

Emergency savings, medical costs, major life events, and retirement all depend on the money available month to month.

Credit cards and lifestyle creep can weaken a plan before they feel obvious.

Reviewing the numbers regularly can help you adjust before small gaps become larger ones.

The Federal Reserve reported that 73% of adults were doing okay financially or living comfortably in 2025, but just above 9 in 10 adults still said price increases were a minor or major concern.[1] That tension is exactly why cash flow and budgeting still deserve attention in 2026.

Habits, Overspending, And What The Budget Reveals

A budget gives you a way to see money coming in and going out instead of relying on memory. That matters because most overspending does not announce itself with one dramatic purchase. It usually builds through habits.

Some of those habits come from higher prices on things you truly need. Groceries, insurance, utilities, childcare, and transportation can change the budget without much choice on your part. Other habits come from convenience, comparison, stress, or the familiar feeling that you have worked hard and deserve something new.

That does not make every purchase wrong. It simply means the numbers should have a say.

Credit cards can make this harder because the purchase and the payment are separated. Tap, swipe, order, subscribe, repeat, and the month can look very different by the time the statement arrives. The Federal Reserve Bank of New York reported that U.S. credit card balances stood at $1.25 trillion in the first quarter of 2026.[2] Credit can be useful when it is managed carefully, but balances and interest charges can crowd out savings, debt reduction, and other priorities.

A budget helps bring those transactions back into focus. It shows whether credit card spending fits within the month, whether the balance is being paid down, and whether interest is taking money away from goals you care about more.

Lifestyle Creep Can Happen Quietly

We live in a world where wants and needs can start to sound very similar. As income grows, spending often grows with it. A nicer trip, a bigger renovation, more dinners out, more subscriptions, more help for family, more convenience. None of those choices is automatically a problem. The problem starts when they become automatic.

Lifestyle creep is tricky because it can happen even when things look fine. You may not be in debt. You may be paying the bills. You may even be saving. But the budget may still show that more income is being absorbed by a lifestyle you never deliberately chose.

This becomes especially important near or in retirement. It is reasonable to want to enjoy the early retirement years, take the trip, remodel the house, spend time with family, or check long-delayed experiences off the list. But those choices need to be measured against the later years too, when healthcare, home maintenance, inflation, and care needs may take up more room in the budget.

That is where cash-flow-based planning earns its place. Goals matter, but the plan also has to show how those goals will be funded year by year. A budget helps answer the question that broad goals alone cannot answer: can this lifestyle be supported for as long as we may need it?

Emergency Savings Gives The Plan Some Breathing Room

Many households live paycheck to paycheck. That can be true for working families, retirees living on Social Security and investment distributions, or anyone dealing with higher costs and limited flexibility. Unfortunately, this leaves little room for the unexpected.

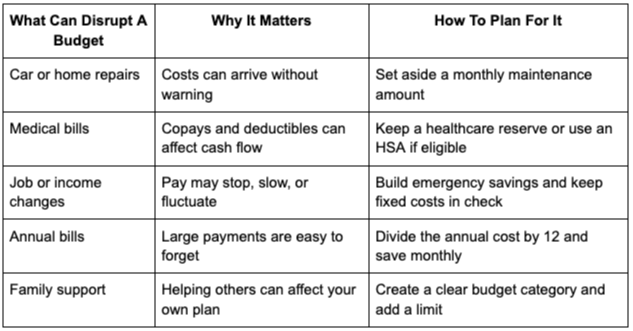

Cars break down. Furnaces stop working. Pets need emergency care. Medical bills arrive. Jobs change. Family members need help. The budget’s job is to make sure some money is assigned to the unexpected before the unexpected shows up.

The Federal Reserve reported that 63% of adults could cover a hypothetical $400 emergency expense using cash or its equivalent in 2025.3 For everyone else, a $400 expense may require borrowing, carrying a credit card balance, selling something, or going without.

An emergency fund can help reduce that pressure. A common guideline is to build toward three to six months of essential living expenses, but the first step can be smaller. One deductible. One repair. One week of core bills. Even a modest reserve can give the household more options.

For retirees, emergency savings may also reduce the need to sell investments at an inconvenient time. That does not remove market risk, but it can give the plan more flexibility when a large expense arrives during a downturn.

Medical Expenses Need Their Own Line In The Budget

Medical costs are hard to predict, which is exactly why they should not be ignored. Premiums, deductibles, copays, prescriptions, dental care, vision care, therapy, medical equipment, and long-term care can all affect cash flow.

Healthcare spending is expected to remain a major pressure point. CMS projects national health expenditures to grow faster than gross domestic product from 2024 through 2033, with health spending rising from 17.6% of GDP in 2023 to 20.3% in 2033.4 Those are national numbers, but households feel the pressure in much more personal ways.

Long-term care is one of the biggest reasons to plan ahead. CareScout notes that 7 out of 10 people will require long-term care in their lifetime, and its 2025 Cost of Care Survey collected more than 25,000 provider rates nationwide.5 Care may happen at home, in assisted living, in a nursing facility, or through a combination of family and paid support. The setting may vary, but the need for a long-term care expense plan remains.

Big Life Events Belong In The Budget Before They Arrive

Some expenses are joyful and stressful at the same time. Weddings, homes, babies, moves, career changes, and retirement transitions all come with decisions that can move quickly and cost more than expected.

Weddings are a good example. The Knot’s 2026 Real Weddings Study reported an average U.S. wedding cost of $34,200 for couples married in 2025.6 That does not mean every wedding should cost that much, but it does show why a wedding budget should include more than the obvious vendor deposits. Travel, attire, gifts, tips, postage, welcome events, and last-minute changes can add up.

Homeownership works the same way. The median sales price of houses sold in the United States was $403,200 in the first quarter of 2026, according to Federal Reserve Economic Data.7 The purchase price is only the beginning. Property taxes, insurance, utilities, repairs, furniture, maintenance, and moving costs all belong in the decision.

Starting a family brings another set of numbers. KFF found that pregnancy, childbirth, and postpartum care averaged $20,416 in total health costs, including $2,743 in out-of-pocket expenses, for women enrolled in employer plans.8 That does not include every ongoing cost that may follow, such as childcare, diapers, formula, clothing, insurance changes, or income changes during leave.

Budgeting does not take the emotion out of these milestones. It helps keep the financial side from taking over the experience.

Retirement Planning Starts With Cash Flow

Budgeting also helps make retirement planning more tangible. An account balance matters, but it does not answer every question. The more important question is what that balance needs to support.

When do you want to stop working full time? When might Social Security begin? Will you stay in your current home or move somewhere with a different cost of living? How much do you want available for travel, hobbies, family, charitable giving, or home projects? What happens if healthcare costs rise, one spouse needs care, or markets are down when withdrawals are needed?

A retirement budget helps test those questions before retirement begins. It can also show whether retirement contributions are in balance with today’s cash flow. Saving more may sound like the right move, but if it forces everyday expenses onto a credit card, your overall financial position may not be improving.

That is why budgeting and doing the math is not only about counting pennies. It is about making an intentional plan for your money that works in real life and helps move you toward your goals.

Frequently Asked Questions About Budgeting

Budgeting often sounds like something people do only when money is tight. In practice, it can help households at many income levels make clearer decisions about spending, savings, debt, and long-term planning.

Do I need a budget if I am not in debt?

Yes. A budget can help you decide where extra cash should go, whether spending matches your priorities, and how prepared you are for future expenses. It is not only a debt-control tool.

Is cash-flow planning different from goal-based planning?

Goal-based planning starts with what you want to accomplish. Cash-flow planning tests how those goals fit with income, expenses, taxes, savings, debt, and timing. The two can work together, but cash flow helps reveal whether the plan is realistic.

How can a budget help with overspending?

A budget shows spending patterns that may not be obvious from memory. Once those patterns are visible, you can decide which categories need limits, which expenses should be reduced, and which purchases are worth keeping.

Why should retirees keep a budget?

Retirees often rely on Social Security, pensions, investment withdrawals, or a combination of income sources. A budget helps track whether withdrawals, healthcare costs, taxes, travel, housing, and family support remain aligned with the retirement plan.

What is the first step if I want to start budgeting?

Start by listing monthly income and monthly expenses. From there, separate fixed bills, flexible spending, irregular expenses, debt payments, and savings targets so you can see the full cash-flow picture.

So Why Do the Math of Building a Budget?

Maybe you are not in debt. Maybe you pay off your credit cards each month. Maybe the wedding, the first house, and the new-baby years are behind you. Maybe, by most measures, you are doing fine.

That may all be true, and budgeting can still matter.

A budget can help you move from “we are fine” to “we are thriving.” It can help you spot habits, prepare for emergencies, understand medical and family costs, and make retirement decisions with a clearer view of your cash flow. It can also help turn a vague goal into a number, a timeline, and a plan.

Sources

1 - Federal Reserve Board, Economic Well-Being of U.S. Households in 2025, May 2026. The report states that 73% of adults were doing okay financially or living comfortably, while just above 9 in 10 adults said price increases were a minor or major concern.

2 - Federal Reserve Bank of New York, “Household Debt Balances Rise Slightly as Delinquency Transition Rates Remain Elevated,” May 12, 2026. The New York Fed reported that credit card balances stood at $1.25 trillion in Q1 2026.

3 - Federal Reserve Board, Economic Well-Being of U.S. Households in 2025 data visualization, “Unexpected Expenses.” The data show that 63% of adults would cover a $400 emergency expense using cash or its equivalent.

4 - Centers for Medicare & Medicaid Services, “National Health Expenditure Projections, 2024-2033.” CMS projects national health expenditures to grow faster than GDP from 2024 through 2033 and the health spending share of GDP to rise from 17.6% in 2023 to 20.3% in 2033.

5 - CareScout, “2025 Cost of Care Survey Results” and “Cost of Care Report.” CareScout reports collecting more than 25,000 provider rates for the 2025 survey and notes that 7 out of 10 people will require long-term care in their lifetime.

6 - The Knot, “This Is the Average Wedding Cost, Backed By Data.” The Knot’s 2026 Real Weddings Study reports an average U.S. wedding cost of $34,200 for couples married in 2025.

7 - Federal Reserve Economic Data, “Median Sales Price of Houses Sold for the United States.” FRED provides median U.S. sales price data for houses sold through Q1 2026.

8 - KFF, “Health Costs Associated with Pregnancy, Childbirth, and Infant Care.” KFF found that pregnancy, childbirth, and postpartum care averaged $20,416 in total health costs, including $2,743 in out-of-pocket expenses, for women enrolled in employer plans.