Small-business loans can help fund equipment, working capital, expansion, real estate, or refinancing, but the right structure depends on how the borrowed dollars will be repaid. For owners and partners, the strongest borrowing decisions usually start with cash flow, documentation, and a clear purpose for the funds. The goal is not simply to get approved; it is to choose financing that fits the business without creating avoidable strain.

Key Takeaways

A small-business loan should be evaluated by structure, repayment terms, flexibility, and total cost, not only by the advertised interest rate. Lenders want to see whether the business can support the payment schedule under normal conditions and still have room for uneven revenue, slower collections, or rising costs.

Match the loan type to the business need and expected payback period.

Prepare current financials before approaching lenders.

Review total cost, covenants, fees, and prepayment terms before signing.

Clarify guarantees and decision rights in partnerships or multi-owner firms.

Compare proposals side by side so the tradeoffs are visible.

Doing the math early gives owners a better view of what the business can reasonably carry. It also helps turn lender conversations from a broad search for capital into a focused discussion about fit.

What Counts As A Small-Business Loan?

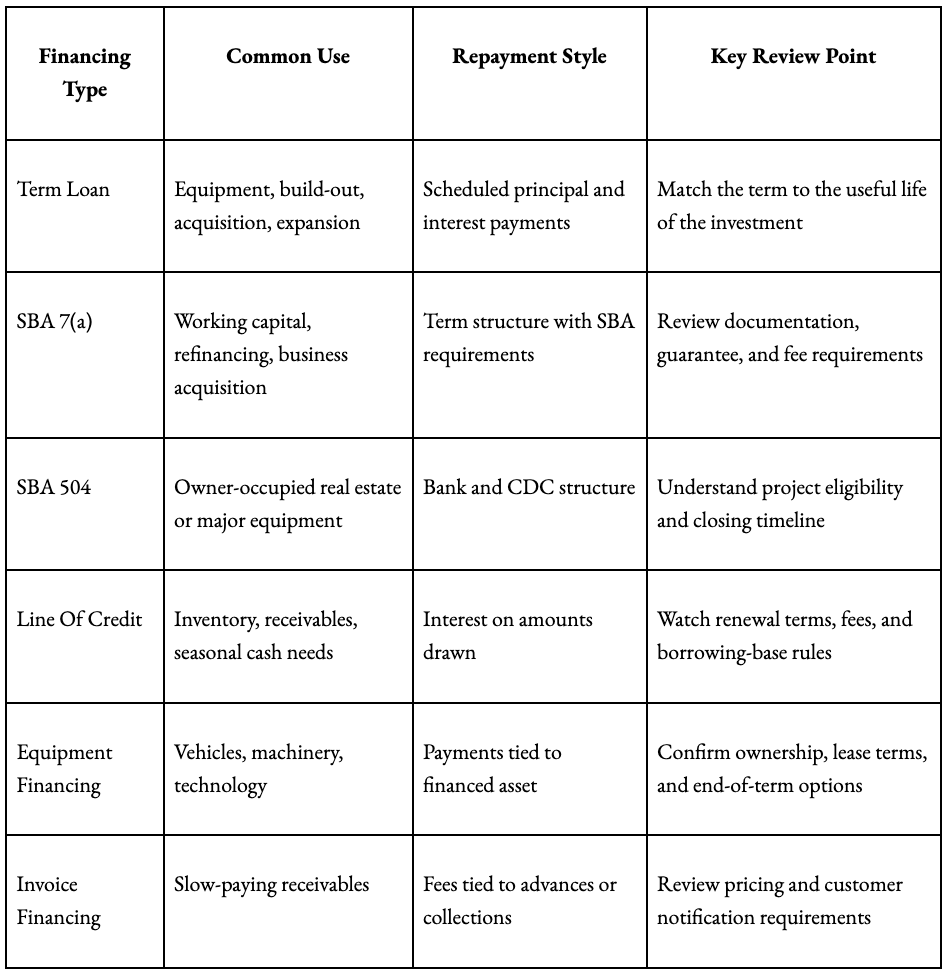

“Small-business loan” is a broad label. It can mean a conventional term loan, an SBA-backed structure, a revolving line of credit, equipment financing, invoice financing, or a real-estate-backed loan. Each option solves a different problem.

A term loan typically provides a lump sum that is repaid over a set schedule. That can work well for equipment, build-outs, acquisitions, or other defined investments where the expected benefit can be tied to a timeline. A business line of credit works differently. It offers revolving access to funds and is often used for inventory, receivables timing, or short-term working capital swings.

SBA loans may be appropriate when a business needs longer repayment terms, broader eligible uses, or a structure that conventional lenders may not offer. SBA 7(a) loans are commonly used for working capital, acquisitions, refinancing, and other general business purposes. SBA 504 loans are more project-specific and are often associated with owner-occupied real estate or major equipment.

Asset-based options are more closely tied to the item being financed. Equipment loans or leases are generally secured by the equipment itself. Invoice financing uses receivables as the borrowing base, which may help bridge collections timing but can carry pricing and administrative considerations that deserve careful review.

How Lenders Decide Small Business Loan Repayment

Lenders are trying to answer one central question: can the business repay the debt on the proposed schedule? That answer comes from more than one number.

Cash flow receives the closest attention. Underwriters review profitability, existing debt, seasonality, customer concentration, and the amount of cushion available after required payments. For many lenders, the strength of the file depends on whether the business can show coverage under a base case and still remain viable if revenue softens or expenses rise.

Credit history also matters. Both business and personal credit may be reviewed, especially when owners are expected to provide personal guarantees. Payment behavior, utilization, liens, judgments, and other public records can influence the lender’s view of risk.

Documentation quality can also affect the process. Clean, current records help the lender understand the business faster. Inconsistent statements, outdated financials, or unclear use of proceeds can slow underwriting and create questions that may have been avoidable.

The Cost Of A Loan Is More Than The Rate

The stated interest rate is only part of the borrowing cost. Fees, amortization, renewal requirements, collateral expectations, and prepayment language can change the practical cost of a loan.

Two loans can have similar rates but very different cash-flow effects. A shorter amortization may reduce total interest but create a heavier monthly payment. A longer term may improve monthly flexibility but increase total interest paid over time. For lines of credit, owners should review draw fees, unused-line fees, renewal fees, and any annual review requirements.

The following comparison can help frame the first round of questions:

The better fit usually aligns repayment with how the business earns the money back. Long-term assets generally need longer repayment schedules. Short-term cash gaps are often better matched with revolving credit that can expand and contract with the operating cycle.

What To Prepare Before Applying For A Small Business Loan

A lender-ready package does not need to be complicated, but it should be complete. Owners who organize the file before outreach often get cleaner feedback and more comparable proposals.

Most lenders will ask for:

Year-to-date profit and loss statement and balance sheet

Two to three years of business tax returns

Accounts receivable and accounts payable aging reports

Current debt schedule

Business formation documents and ownership details

Personal financial statements and tax returns for guarantors

Project quotes, purchase agreements, or construction budgets

A short use-of-proceeds summary explaining how the funds will be used

That last item matters more than many owners expect. “Working capital” may be accurate, but it may not be specific enough. A stronger explanation connects the requested funds to inventory timing, hiring needs, expansion costs, receivable delays, or another identifiable business purpose.

If you are weighing a financing decision and want another set of eyes on the structure, contact the office before you begin lender conversations. A cash-flow review can help clarify how much borrowing capacity the business may be able to support and which questions should be answered before documents are signed.

Special Issues For Partners And Multi-Owner Businesses

Partnerships and multi-owner firms add another layer to underwriting. The lender may want to know who can authorize borrowing, who signs the loan documents, who guarantees the debt, and how distributions affect available cash flow.

Governance documents should be current and consistent with the proposed financing. Operating agreements, partnership agreements, corporate resolutions, and signer authority should be reviewed before closing pressure builds. If one owner is leading the process, the lender may still need information from all guarantors.

Distribution policy is also important. A business can show profitability on paper while still leaving too little cash inside the company to support debt service. Lenders may ask how owners decide when to take distributions and whether those payments could be reduced if the loan requires more cash to remain in the business.

Comparing Small Business Lenders Without Losing The Big Picture

A broad search can create confusion if each lender receives different information. A more disciplined approach is to prepare one core packet and send it to a short list of lenders that understand the industry, project type, or collateral.

When proposals come back, compare them across the same categories. Rate belongs in the review, but it should sit next to fees, amortization, collateral, guarantees, covenants, prepayment terms, and reporting requirements.

Pay close attention to covenants. Minimum liquidity, leverage limits, debt service coverage, and reporting deadlines can affect how the business operates after funding. A loan that looks attractive at closing may feel restrictive if the business later needs flexibility.

Prepayment language deserves the same level of review. Some loans include penalties or specific windows for early payoff. That may matter if the business expects to refinance, sell an asset, bring in new partners, or adjust debt as conditions change.

Deciding On A Small Business Lender

When several options appear workable, bring the decision back to three points: purpose, payback, and protections.

Purpose defines the reason for borrowing. The more specific the purpose, the easier it is to evaluate whether the amount and structure make sense.

Payback connects the financing to cash flow. Owners should look at the expected payment under normal conditions and then test what happens if revenue is lower, collections slow, or expenses increase.

Protections include the boundaries around the loan. Covenants, guarantees, collateral, reporting requirements, and prepayment terms all affect the business after the money is received.

If those three pieces align, the financing may be worth further review. If one piece feels strained, the better answer may be a smaller loan, a different term, a delayed project, or a different funding source.

Frequently Asked Questions About Small Business Loans

Small-business financing decisions often raise practical questions before an application is submitted. The answers below reflect the main issues owners and partners should review when comparing loan options.

How Much Can A Small Business Borrow?

Borrowing capacity depends on cash flow, collateral, existing debt, owner guarantees, credit history, and the lender’s underwriting standards. Many lenders focus on whether projected payments fit within the company’s available cash flow rather than using one fixed borrowing formula.

Is An SBA Loan Better Than A Conventional Loan?

An SBA loan may be useful when longer terms, broader uses, or more flexible collateral requirements are important. A conventional loan may be more efficient when the business has strong cash flow, solid collateral, and a straightforward request.

What Documents Should Be Ready Before Applying?

Owners should gather current financial statements, recent business tax returns, aging reports, a debt schedule, ownership documents, guarantor information, and a clear use-of-proceeds summary. Project-specific requests may also require quotes, purchase agreements, budgets, appraisals, or insurance information.

Do Business Owners Usually Have To Personally Guarantee The Loan?

Many small-business loans require personal guarantees, especially when the business is closely held or has limited collateral. In multi-owner firms, the lender may require guarantees from more than one owner depending on ownership percentages, risk, and loan structure.

Why Does The Loan Term Matter?

The term affects both monthly payments and total borrowing cost. A term that is too short can pressure cash flow, while a term that is too long may increase total interest and reduce flexibility.

What Should Seasonal Businesses Show A Lender?

Seasonal businesses should provide month-by-month financials and a clear explanation of revenue timing, expense cycles, collections, and off-season cash needs. That context helps the lender separate normal seasonality from repayment risk.

The Bottom Line On Small-Business Loans

Small-business loans can support growth, stability, and transition when the structure fits the purpose and the repayment plan fits the cash flow. Owners and partners should compare total cost, documentation requirements, covenants, guarantees, and prepayment terms before choosing a lender. The best starting point is to do the math, define the purpose of the funds, and pressure-test the payment schedule before committing. For deeper analysis or a second set of eyes on options, contact the office to schedule a meeting with your financial professional today.